A simple lesson worth sharing: The power of compound interest.

Compound interest is the quiet engine behind long-term investing — the idea that your interest earns interest, creating growth on top of growth over time.

Watch this Episode

Listen to this Episode

Subscribe to Vector’s Well Balanced podcast on Apple Podcasts or Spotify for weekly market updates and real-world financial planning topics. Including this episode.

Some lessons are too valuable to keep to ourselves.

If there’s someone in your life—a child, grandchild, or friend—who’s just beginning to save or invest, consider passing along this episode of Well Balanced. Vector Wealth Advisor David Moser shares a simple, yet powerful illustration of how compound interest turns small, consistent investments into lasting wealth over time.

Even for those already living off their portfolios, it’s a powerful reminder of why time and consistency matter.

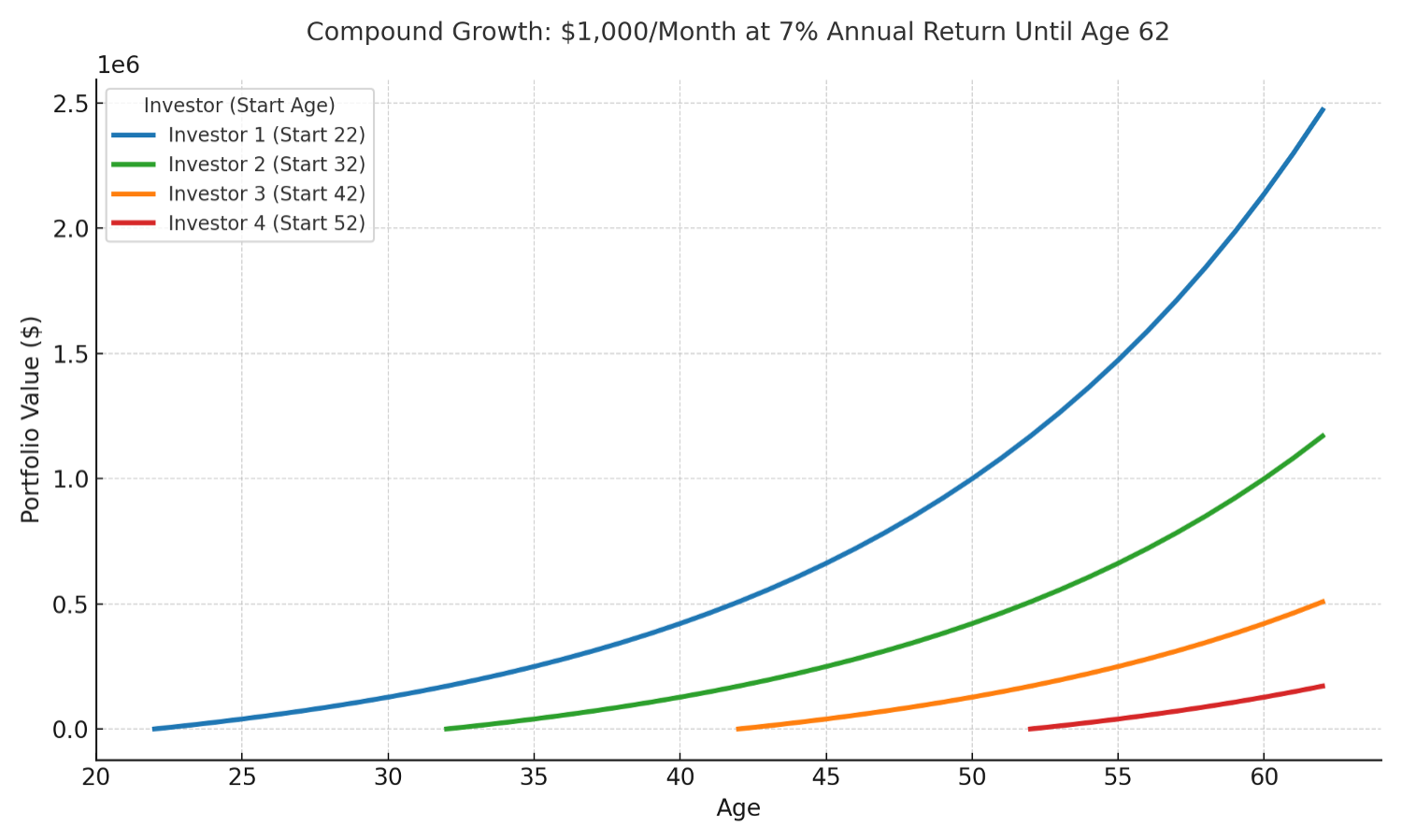

In David’s story, four friends each invest $1,000 per month, earning the same, for illustration purposes, 7% annual return but starting at different ages:

· At 52, the total grows to about $170,000 after 10 years.

· At 42, roughly $520,000 after 20 years.

· At 32, over $1.1 million after 30 years.

· At 22, about $2.5 million after 40 years.

Each invests the same monthly amount—but the ones who start earlier let time do most of the work.

It’s a great reminder for all investors: compound interest rewards patience, not perfection.

💡 Share this episode with someone who could use a head start—or a fresh perspective—on the power of saving early.

Chapters

0:25 … Introduction to Compound Interest

1:44 … The Scenario

3:02 … Comparing Outcomes

4:30 … The Hockey Stick Effect

5:21 … Key Takeaways and Action Steps

5:56 … Regulatory

Transcript

(Adapted for readability)

Introduction to Compound Interest

Hi everyone, my name is David Moser and I am one of the wealth advisors at Vector Wealth Management. Today, we’re going to talk about one of the most powerful and often overlooked forces in investing: compound interest. Compound interest is a simple concept, but its impact is extraordinary. Once you see it in action, it completely changes how you think about saving and investing for retirement.

So, what is compound interest? It means the interest on your investments earns interest. Imagine four friends: Jim, John, Sarah, and Amanda. They all invest the same monthly amount—$1,000 per month—and all plan to retire at age 62. They invest in the S&P 500, earning the same 7% annual return. The S&P 500 is comprised of the largest 500 publicly traded companies in the US. Over the last 100 years, the S&P has averaged almost 11% per year, but past performance isn’t indicative of future returns. For conservative purposes, let’s assume all friends earn 7% per year.

There can be no assurance that any specific investment or investment strategy will be suitable for a client’s or prospective client’s investment portfolio. Various indexes have been chosen that are generally recognized as indicators or representation of the stock market in general. Indices are typically not available for direct investment, are unmanaged and do not include fees or expenses.

The Four Friends Scenario

This example isn’t saying that investing $1,000 a month is enough to achieve retirement goals, as everyone’s financial situation is different. This is a simple math exercise to demonstrate the power of time and compound interest. For those listening on audio, I’ll describe the chart posted to our blog.

The chart shows four curved lines—red, orange, green, and blue—each representing a different starting age. As you move from right to left, you see what happens when someone starts investing earlier. The curves rise faster and higher, showing the power of compounding at work: growth on growth. Let’s start with Jim.

Jim starts investing for 10 years at age 52. By the time he retires at 62, he has contributed $120,000 of his own money. His portfolio grows to around $170,000. That’s not nothing, but it might mean Jim needs to keep working longer or save more aggressively to reach his ideal retirement lifestyle.

Comparing Investment Outcomes

John starts investing at age 42, ten years earlier than Jim. He invests for 20 years, contributing $240,000 of his own money. His balance at 62 is a little more than double Jim’s, at roughly $520,000.

Sarah starts investing at age 32, giving her a 30-year timeframe. She contributes $360,000 of her own money, and by age 62, her portfolio grows to about $1.1 million. Now we see real growth acceleration. Her line on the chart, the green one, curves sharply upward near retirement age.

Amanda starts investing at age 22. She invests for 40 years, contributing a total of $480,000—just $120,000 more than Sarah. Over 40 years, her portfolio grows to $2.56 million by age 62. That’s more than double Sarah’s outcome and roughly 15 times what Jim accumulated, all by starting earlier.

The Hockey Stick Effect

The chart shows Amanda’s line shooting almost straight up near the end—what we call the hockey stick effect. That’s the beauty of compound growth: slow and steady for years, then suddenly it takes off. If you’re listening on audio, you can find the same chart on our blog at vectorwealth.com.

To summarize: the earlier you start, the more your money and your time work for you. Compound interest rewards time in the market, not timing the market. Albert Einstein once said compound interest is like the eighth wonder of the world. The lesson is simple: the best time to start investing was yesterday, and the second best time is today.

Key Takeaways and Action Steps

No matter your age, the principle remains the same: stay consistent, stay invested, and let compounding work for you. Markets don’t move in a straight line, but over time, consistency, discipline, and patience win. Whether you’re 25 or 75, the math of compounding interest works, and the sooner you begin, the more powerful it becomes.

If you’d like to see how compound interest can impact your own financial goals, feel free to reach out to our team at Vector Wealth Management.

Contact Us or Schedule an Intro Call

These discussions aim to spark dialogue about enhancing retirement readiness and making more informed financial decisions. At Vector, we delve into the nuances of scenario planning, offer insights and guidance tailored to each client's unique circumstances. If you or someone you know is pondering their financial future or seeking clarity on their retirement plan, we're here to help.

Disclosures

Information expressed does not take into account your specific situation or objectives, and is not intended as recommendations appropriate for any individual. This material is not intended as, nor should it be relied upon for, tax, legal, or accounting advice. Always consult your own tax, legal, and accounting advisors before making decisions or implementing strategies. Listeners are encouraged to seek advice from a qualified tax, legal, or investment adviser to determine whether any information presented may be suitable for their specific situation. Past performance is not indicative of future performance. Investments involve risk and unless otherwise stated, are not guaranteed.

V25300287